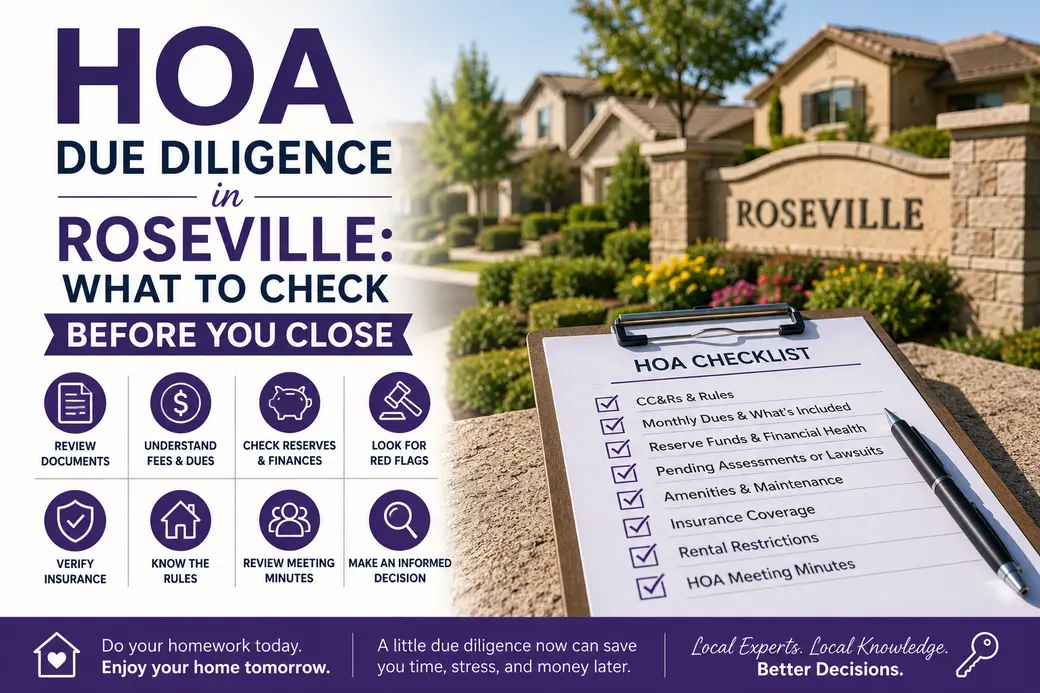

HOA Due Diligence in Roseville: What to Check Before You Close

What should you review before buying a home in a Roseville HOA community?

Before you close on any Roseville home with an HOA, review the CC&Rs, current financials, reserve study, and at least 12 months of board meeting minutes. The single most important number is the reserve fund percentage — anything below 50% is a red flag for future special assessments. Under new 2026 California law, sellers must also disclose exterior elevated element inspection reports for any HOA with decks, balconies, or walkways. The best time to ask all your questions is during your contingency period, before you sign off on the HOA documents.

By Rich & Kat Farless | June 29, 2026

Most buyers spend hundreds of dollars on a home inspection and virtually nothing on HOA due diligence. That's backwards. Because while a broken water heater costs a few thousand dollars to fix, buying into an HOA with underfunded reserves or a surprise special assessment can cost you tens of thousands — and you won't find out until after you've already closed.

If you're buying a home in Roseville, Granite Bay, Folsom, Lincoln, or any of the newer West Roseville communities — and especially if you're looking at Placer One, Amoruso Ranch, or Fiddyment Farm — here's what you need to check before you sign off.

What Documents Does the Seller Have to Give You?

Under California's Davis-Stirling Common Interest Development Act, the seller of any home in a common interest development (CID) — that includes planned communities with HOAs — is required to provide you with a mandatory disclosure package. You get it during escrow, and you have three business days after receiving it to review everything. If you don't like what you see, you can back out without losing your earnest money — but only if you haven't already removed your HOA contingency.

The package must include:

- CC&Rs (Covenants, Conditions & Restrictions) — the legally binding rules that govern what you can and cannot do with your property

- Bylaws — how the HOA is governed and how decisions are made

- Current financials — the HOA's operating budget and balance sheet

- Reserve study — a long-range capital planning report (more on this in a minute)

- 12 months of board meeting minutes — your clearest window into what the board has been dealing with

- Insurance certificate — what the HOA master policy covers

- Pending litigation disclosure — any active lawsuits involving the association

New for 2026: Under Senate Bill 410, sellers must now include exterior elevated element inspection reports — specifically the SB 326 balcony and walkway inspection results — in the disclosure package. If your HOA has decks, balconies, or elevated walkways and hasn't completed an inspection, that failure to inspect is itself a material disclosure. For condos and townhomes in particular, read this report carefully.

The seller pays the HOA transfer fee to prepare and deliver this package. In California, those fees typically run $200 to $500, though some associations charge more. That cost hits the seller's side of the closing statement — it's one of the line items in the standard seller closing cost breakdown.

The Reserve Fund: The Number That Tells You Everything

Here's the most important thing you're going to look at in those financials: the reserve fund percentage.

A reserve study estimates the remaining useful life of every major component the HOA is responsible for — roofing, exterior paint, plumbing, pool equipment, community structures, elevators if applicable — and projects how much money the association needs to set aside to replace those components over time. The reserve fund percentage tells you how close the association is to being fully funded.

General benchmarks:

- 70% or above — healthy. The association is well-positioned to handle capital repairs without emergency measures.

- 50%–70% — watch closely. Not a dealbreaker, but ask the board what the plan is to close the gap.

- Below 50% — red flag. An underfunded HOA is more likely to raise dues, pass special assessments, or defer maintenance until it becomes an emergency.

California law limits special assessments to 5% of the HOA's annual budgeted gross expenses without a member vote. For a larger association with a $500,000 annual budget, that's $25,000 — potentially several thousand dollars per unit, collected in a lump sum. Boards can exceed the 5% cap, but only with a majority vote of a quorum of members. Emergency situations — structural safety issues, court orders, and utility infrastructure failures — can bypass the vote requirement entirely.

Real numbers from Sacramento: One Campus Commons townhome owner saw monthly HOA fees climb from $275 in 2015 to $562 a month by 2026. Those increases weren't arbitrary — they reflected years of deferred maintenance catching up with an underfunded reserve.

When you're reviewing the HOA package, ask:

- Has the HOA ever passed a special assessment? If so, what triggered it, how much, and when?

- Are any special assessments being discussed or planned?

- Is the board currently funding reserves at the level the reserve study recommends?

What the CC&Rs Actually Mean for Your Daily Life

The CC&Rs are where buyers get surprised — sometimes unpleasantly. These are legally binding restrictions tied to your title. When you close, you agree to follow them whether you've read them or not.

Things the CC&Rs may restrict:

- Rental restrictions — many Roseville communities prohibit short-term rentals (Airbnb/VRBO) entirely, and some limit the number of long-term rentals allowed in the community at any given time. If you ever plan to rent the property, read this section carefully.

- Exterior modifications — paint colors, additions, landscaping, fencing, and satellite dishes often require HOA architectural committee approval.

- Parking — restrictions on RVs, boats, commercial vehicles, and even the number of cars parked on the street.

- Pets — breed restrictions and size limits are common.

New for 2026: Under Assembly Bill 130, HOAs are now prohibited from enforcing fines over $100 unless there's a documented health or safety issue. This is a meaningful protection for homeowners — but it doesn't make the CC&Rs themselves less binding. You still can't paint your house neon yellow without approval; the HOA just has more limited financial recourse if you do.

Also new: Senate Bill 625 (effective 2025) ensures that HOAs cannot block you from rebuilding your home after a declared disaster. Following California's wildfire events, this law overrides any outdated CC&R language that might have otherwise prevented reconstruction.

One Roseville-specific note worth knowing: Winding Creek has no HOA. That's unusual for a newer master-planned community in West Roseville, and it's one of the things that makes Winding Creek appealing to buyers who want to avoid association governance entirely. Placer One, by contrast, does have an HOA — it's California's first all-electric master-planned community, with six parks and a sustainability-focused mandate built into its governing structure. Neither is better or worse universally — they're different ownership experiences.

HOA vs. Mello-Roos: The Distinction Roseville Buyers Confuse Most

These are two separate things, and they show up on two different line items.

HOA fees are charged by a private homeowners association and typically cover landscaping of common areas, maintenance of community amenities (pools, parks, clubhouses), and the shared insurance policy. They go to a private entity.

Mello-Roos is a special tax — specifically a Community Facilities District (CFD) assessment — levied by a local government agency to fund the public infrastructure in new communities: roads, schools, parks, sewer systems. It shows up as a line item on your annual property tax bill, not in your HOA dues.

A home in West Roseville can have Mello-Roos with no HOA (like some Winding Creek properties), an HOA with no Mello-Roos (less common in new construction), both, or neither. When you're calculating your true monthly cost of ownership, you need both numbers. We break down exactly how Mello-Roos affects your monthly payment in What Is Mello-Roos? A Roseville New Home Buyer's Guide.

For the big-picture side-by-side on new construction versus resale payment math — including HOA and Mello-Roos — see New Construction vs. Resale in Roseville: What Your Monthly Payment Actually Looks Like.

When to Ask All This — and What Your Contingency Protects

California's Residential Purchase Agreement (CAR RPA) includes an HOA document review contingency as part of the standard contract. Once the seller delivers the mandatory HOA disclosure package, you have three business days to review everything. During that window, you can cancel the contract and recover your earnest money — no penalty.

If you remove your contingencies before the HOA documents arrive (or before you've actually read them), you lose that protection. Your earnest money becomes hard, and if you back out later, the seller may be entitled to keep it.

The practical advice: request the HOA documents as early in escrow as possible. Don't wait until the contingency deadline is looming. We've seen buyers try to review hundreds of pages of CC&Rs, financials, and reserve studies in 48 hours — that's not the kind of reading you want to rush.

For a full picture of what happens in your escrow timeline from offer acceptance to close, see What Happens After Your Offer Is Accepted in Roseville?.

Frequently Asked Questions

Does every home in Roseville have an HOA? No. Older neighborhoods in central Roseville and parts of Rocklin were built before master-planned HOA communities became standard, and some newer West Roseville communities like Winding Creek were specifically designed without one. When you're shopping for homes, check the listing for HOA dues — if there are none listed, verify with your agent whether there's a mandatory association or not.

What is a reserve study and why does it matter? A reserve study is a long-range financial planning report that estimates when major HOA-maintained components — roofs, pools, common area structures — will need to be replaced, and projects how much money the association needs to set aside each year to cover those costs. California law requires HOAs to conduct reserve studies regularly. A reserve fund below 50% is a meaningful warning sign that the association may need to raise dues or levy special assessments in the near future.

Can a California HOA charge unlimited special assessments? No. California Civil Code §5605(b) limits emergency or unilateral special assessments to 5% of the HOA's annual budgeted gross expenses. Beyond that threshold, the board must get a majority vote from a quorum of members. True emergency situations — threats to health and safety, court orders, or utility infrastructure failures — can bypass the vote requirement, but the board must document the emergency.

What is the HOA transfer fee and who pays it? The HOA transfer fee (sometimes called a resale certificate fee or estoppel fee) covers the administrative cost of preparing your disclosure package and updating the association's ownership records. In California, this fee is typically paid by the seller and ranges from $200 to $500+, depending on the association. It's separate from the HOA dues you'll owe starting the month you close.

What's the difference between Mello-Roos and an HOA? A homeowners association is a private entity that maintains shared community amenities and enforces CC&Rs — you pay it monthly or quarterly dues. Mello-Roos is a government-levied special tax (Community Facilities District assessment) that funds the public infrastructure — schools, roads, parks, sewer — in newer communities. It appears on your property tax bill, not in your HOA dues. Many West Roseville homes have one, the other, or both.

The Bottom Line

Most buyers spend the most attention on the inspection report. The HOA documents deserve just as much. The CC&Rs control your ownership rights. The reserve fund predicts your future costs. The board minutes tell you what's actually happening in the community. And the new 2026 California disclosure requirements mean you're now entitled to more information than ever — but only if you actually read what you're given.

If you're buying in a Roseville HOA community and want someone in your corner who knows these documents cold — and knows which West Roseville communities to watch out for — we're here.

Schedule a free consultation at richandkatsoldthat.com/talktous

About the Authors

Rich and Kat Farless are a husband-and-wife real estate team with over 30 years of combined experience serving buyers and sellers across the Sacramento region. As the #1 husband-and-wife team in Roseville, CA, they specialize in single family, new construction, and luxury properties across Placer, Sacramento, and El Dorado counties. Connect with them at richandkatsoldthat.com.

Categories

- All Blogs (31)

- Buyer Resources (1)

- buyers (2)

- Buying a Home (10)

- Buying a Home, New Construction, Placer County, Roseville (1)

- California Real Estate (1)

- California Real Estate Process (5)

- Costs & Finances (1)

- First-Time Buyers (1)

- HOA (1)

- Home Financing (1)

- New Construction (2)

- placer county (1)

- Real Estate Process (1)

- Roseville Real Estate (4)

- Seller Resources (1)

- sellers (1)

- selling a home (5)

Recent Posts

Agent | License ID: 01193836, 01186753

+1(916) 284-1520 | kat@homesbyrichandkat.com